Because DAKSH is reliant on judicial data, we are only able to see how a case was closed. This means, we cannot comment on whether the case was appealed to the Supreme Court or if the judgment was complied with. The eventual result, of properly assessed due-taxes being paid to the assessing authority, is even further beyond the scope of this data.

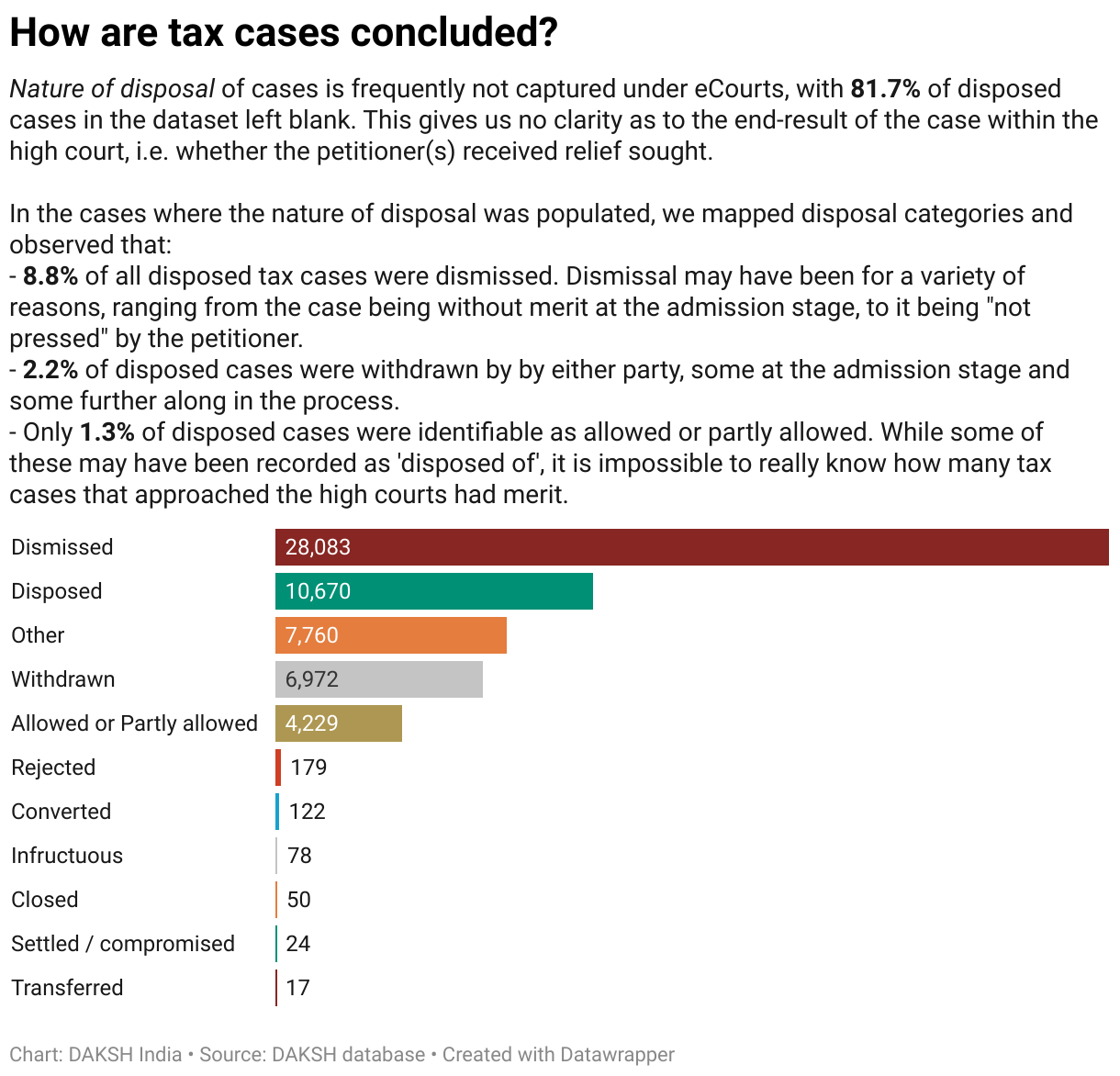

While these categories of disposal aren’t significant within our dataset, some tax cases may be outright rejected or converted to other kinds of petitions. Others may be declared infructuous, wherein the cause of action is no longer relevant; for example, infructuous cases may be related to tax types that have been abolished.

In general, the outcome of a case is clearer with the context of the party or parties that brought the case and what relief they sought. To say that a case was ‘dismissed’ or ’allowed’, has meaning, when it is considered alongside the prayer within the petition.

Due to the major variations and lack of clarity on how disposed cases are marked as such within eCourts, we are currently running a manual exercise to study a sample of final judgments in tax cases. Our aim is to see how each case was actually disposed of and whether relief was granted. We believe this will yield insights into how high courts treat tax matters based on different dimensions. We hope to update this dashboard with our results.

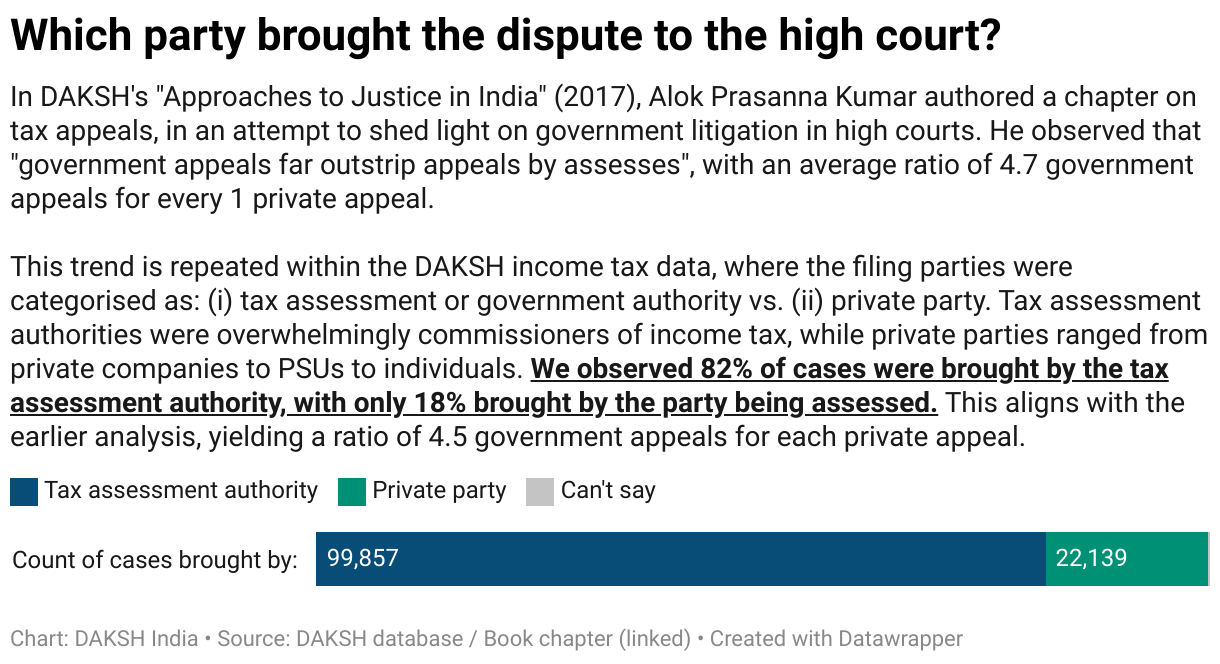

While we cannot access the individual relief/prayers for the tax cases, we conducted a mapping of the petitioner and respondent parties for Income Tax cases.

Judicial data yields valuable insights, however, any effort at meaningful institutional and policy reform requires engaging with stakeholders in the system.

Over the coming months, we will be planning a series of discussions and round-tables to meaningfully engage with the current state of tax litigation and document how it may be reformed. Please reach out to smita@dakshindia.org or info@dakshindia.org to share your experience with tax litigation, whether before tribunal or courts, and register your willingness to be a part of this conversation.