Taxes are the lifeblood of a country’s economic infrastructure, enabling the government to fund essential services, public goods, and sustainable development. Despite the overarching importance of taxation, it is important to bear in mind that the administration of taxes including the dispute resolution process need to balance revenue facilitation with principles of fairness and non-arbitrariness.

Tax litigation thus becomes a barometer for assessing the health of the tax administration system. The likelihood of tax disputes ending up in litigation has a significant impact on the ease of doing business, directly influencing the business environment in the country. When companies and firms face prolonged and complex tax disputes, it can create uncertainty and hinder their operations. The constant threat of litigation also deters potential investors and entrepreneurs. Lengthy legal battles also consume valuable resources, both in terms of time and money, diverting attention away from core business activities.

Preferred citation: DAKSH India (2024). DAKSH High Court Database: Tax Case dataset.[url]

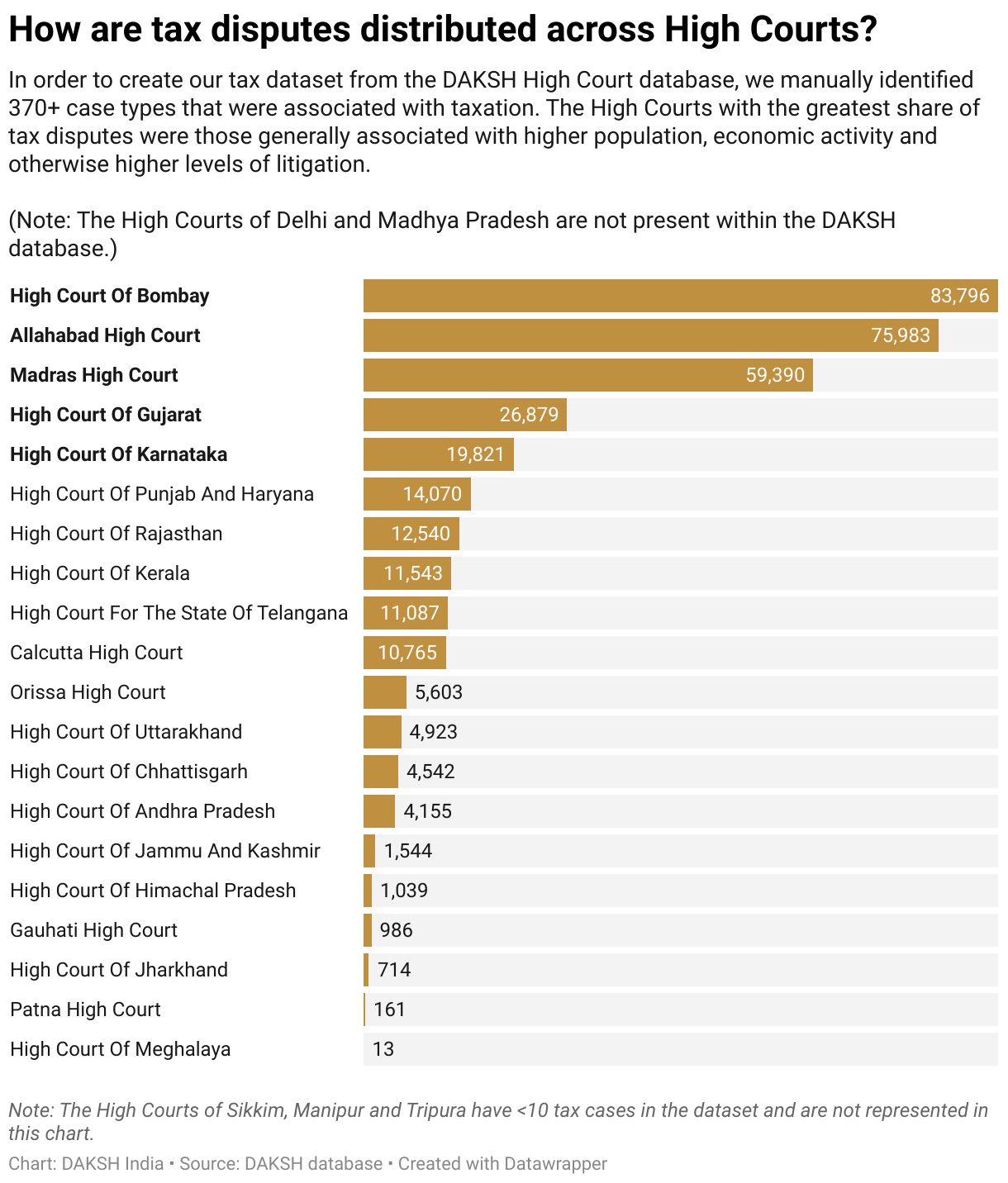

DAKSH’s work on understanding case types goes back to the State of the Indian Judiciary (2016) and Deciphering Judicial Data (2020) reports. They examined over 4,800 unique case typesused by District Courts across India and advocated for the need to harmonise them, to allow court administration, lawyers, and litigants to better understand what kinds of cases come before the judiciary. The same challenges pointed out in those studies are faced in analysing tax cases over the last two decades – namely, that case types differ widely between High Courts and vary over time, with new types being introduced and old ones dropping out of use. Out of the 373 tax-related case types that we manually identified through eCourts services, 212 (just under 57%) were represented in our dataset of cases filed between 2000 and 2021.

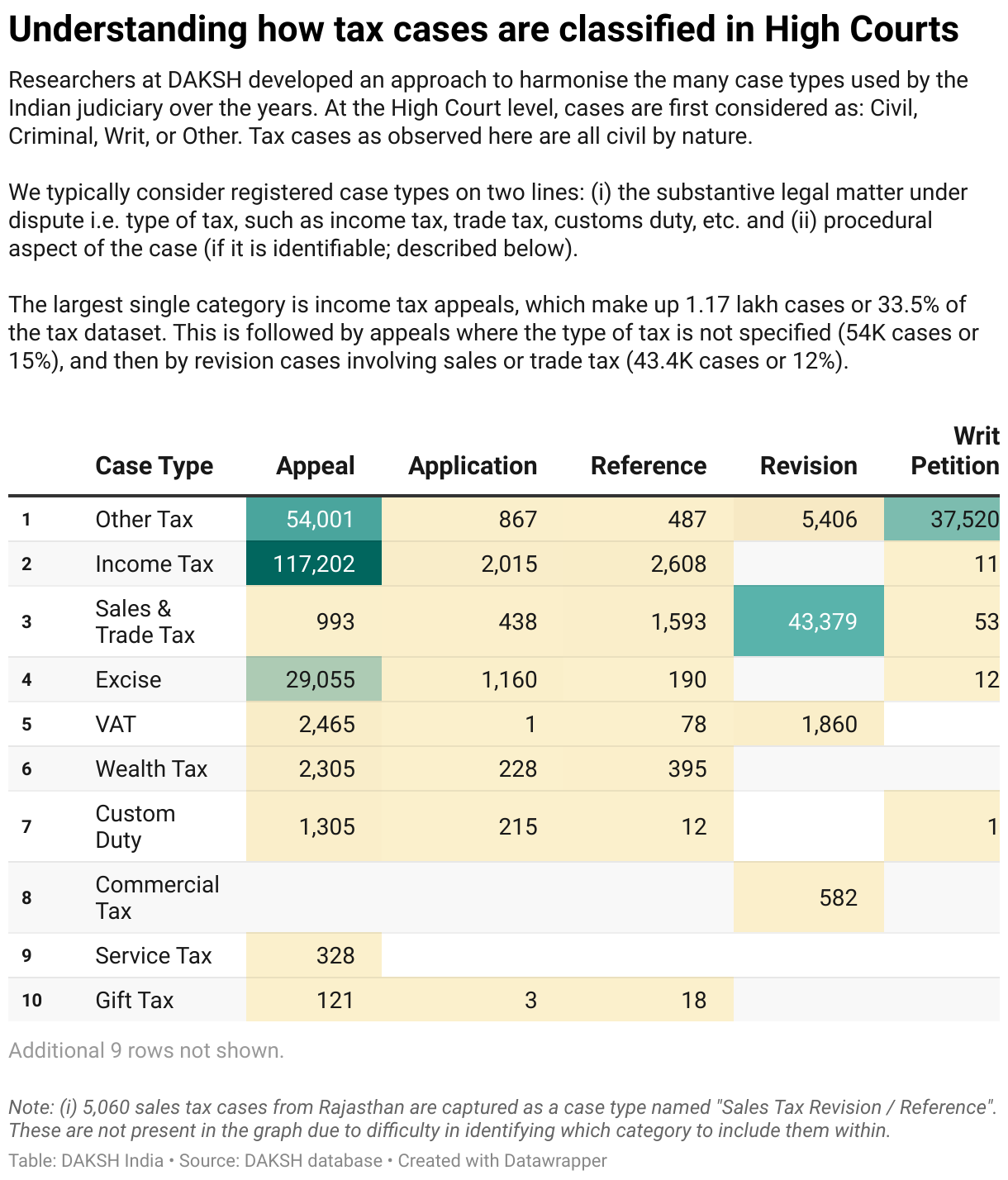

As demonstrated before, cases were categorised based on whether the nature of the tax was direct, indirect, or if we were unable to say from the case type description. Expanding on the procedural focus of disputes outlined above:

Appeals may be identified as cases that appeal the tax assessment calculated or an order given by a tax authority. However (where identifiable), Applications, reference or revisions may be connected with other main matters and potentially represent an inflated total count of active or pending cases present in the system. They may in essence, not constitute a ‘whole’ tax dispute but rather a question of law being raised separately to be heard by a competent judge. The same is true for case types tagged as ‘transfer’, which are not identifiable in our tax dataset.